First-Generation Money

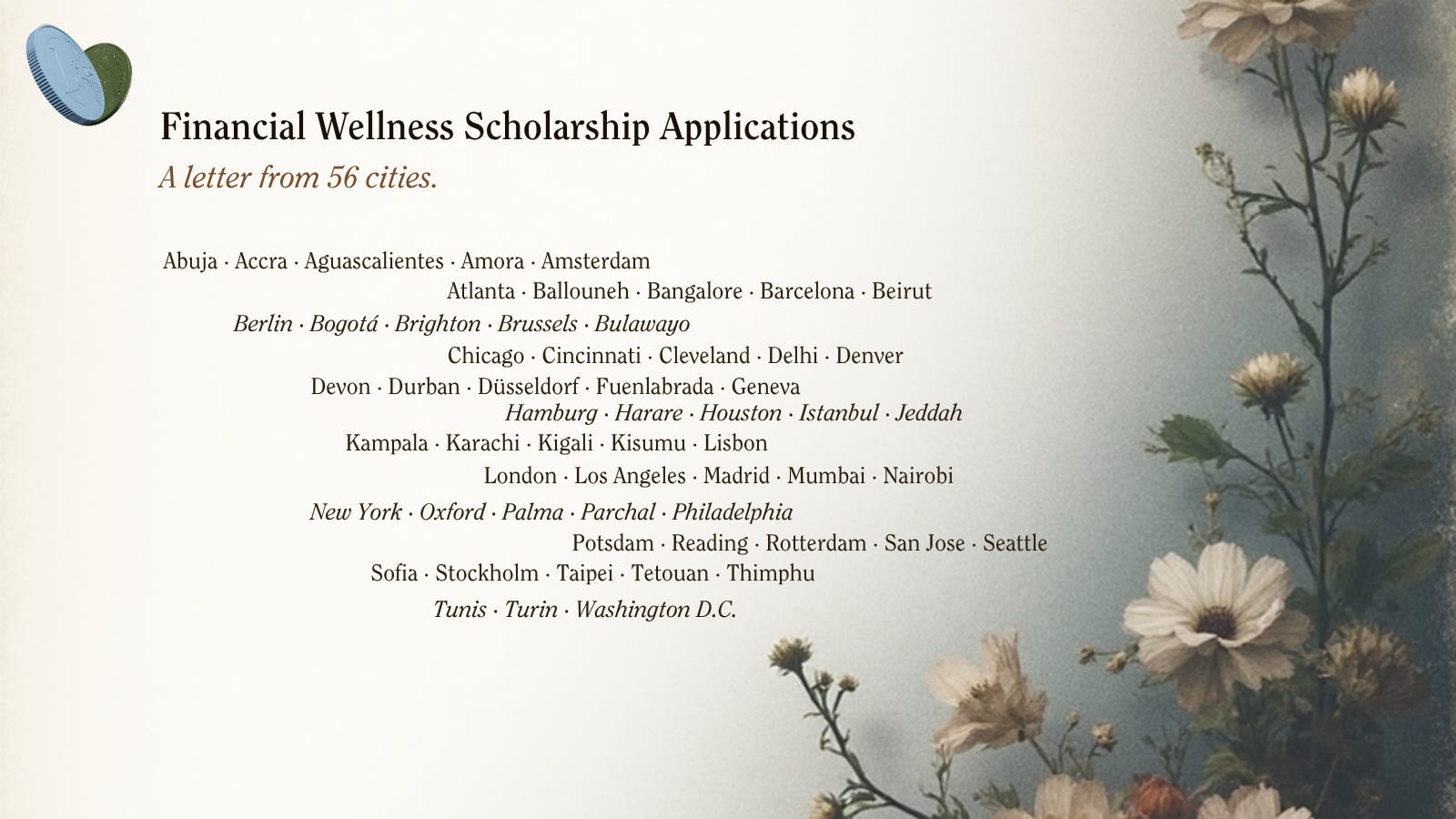

114 stories, 56 cities, 5 continents: true money stories

“My grandmother, one of the strongest influences in my life, never had a bank account.”

She is in her 30s now. A PhD student. The director of a global organisation working on sexual and reproductive health and rights. And, in her own words, “the first generation in my family to navigate financial systems independently.”

She was the winner of the Bloom Financial Wellness Scholarship, and one of 114 people who applied for our April cohort, from 56 cities in 31 countries across five continents (!). I read every single one, from Karachi, Kampala, Cincinnati, Bhutan, Bogotá, Berlin, Beirut, Bulawayo. In fact, the applications were so incredible, we decided to run the scholarship one more time for our June cohort, applications open until 15 May here.

We proudly serve all people who need support in transforming their relationship with money. But this scholarship is specifically for those in social change work and who need the help the most.

I wanted to share some of their stories here, so we normalize talking about money and how it affects us in much bigger ways than we think. I think we can all see ourselves in some ways in these examples.

One clear thread that came up again and again:

Being the first.

Many people who applied were first in family to go to university. First-generation immigrant. First in family to finish secondary school. First woman in family to hold finances independently. First to break a cycle of violence. First in family to migrate.

First-Generation Money

When I was looking for financial advice and guidance years ago, I hit a wall. It felt to me like most content out there was aimed at people who have a basic history with money already. Whose financial life is a series of small refinements on a route somebody else already walked in their family.

Many of you are not that, and this letter is for you. You are people figuring it out yourself. What is incredibly hard about carving a path is that you cannot see it in front of you. You don’t know what it looks or feels like. All you know is that you are moving away from something hard and towards something hopefully better. It takes profound courage to be first.

“I am the first one through this door”

Let me show you a little of what I mean. The stories below are real. While names are removed for privacy; locations are accurate and quotes are their own words:

A university graduate in Amsterdam writes, “as the first person in my family to go to university, I have had little access to financial knowledge or guidance.” She grew up watching her mother remain in a violent relationship because she did not have her own money. She is now the one breaking that pattern.

A first-generation American in Washington D.C. writes, “I grew up in a first-generation, low-income, working-class immigrant family, where I assumed we were ‘rich’ or ‘well off’ because my parents bought us everything we wanted.” She now covers their living expenses.

Someone who lives between the UK and Madrid writes, “I am a first generation university graduate. I come from a low-income background where money was always a stress. My dad claimed bankruptcy when I was a teenager and our family home was repossessed.”

A young woman in Costa Rica writes, “I am the first one to finish secondary school and university, the lack of generational wealth and its impact is quite clear.”

Migration as the ultimate “first”

Migration came up again and again. The truest trailblazers, in many ways, are the ones who left.

A two-time immigrant in Atlanta, Eritrean, who lived half her life in Saudi Arabia, writes, “I have no idea how to approach money. Am I supposed to strive to just survive? Am I supposed to take the big risks for big rewards? Do I even belong in spaces of financial stability?”

A female immigrant in Berlin, writes about a single-income household where her mother held the finances “unheard of in a patriarchal society,” and how she now struggles to keep her own progressive values intact while letting herself spend with joy.

And finally, a profound example from Houston:

“I grew up in a working class family and know how to manage being poor. The challenge comes where I want to improve my financial situation, not just manage.”

This part: I know how to manage being poor. That is the wall. Managing scarcity is a skill you've already mastered. Building something from it is a different muscle. That is what we built DearMoney for.

What being “first” actually costs you

Last month I wrote about the friendship account and the long, ancient lineage of women pooling resources in chamas, seettu, sou-sou, esusu, and tandas. That letter was about what is possible when we organise our financial lives in community.

This one is about the cost of doing the opposite. Of having to do it alone. Besides having to financially start from behind, there are other costs that people pay for being first in their community or family:

It costs in legitimacy. The sense that you are allowed to think about money, ask questions out loud, sit at the table in a financial advisor’s office, fill out a form that asks about pensions without freezing. Almost every first-generation applicant I read described a flicker of “this is not for me” the first time they looked at finances.

It costs in permission. To want financial security without feeling like you are betraying the people who did not have it. Many applicants describe a complicated guilt about earning more than their mother ever did, or about spending on themselves while family back home is stretched thin.

And it costs you a peer. The one thing almost every person who inherited a map has, and most first-generation people do not: someone who knows what it feels like to do this from scratch, in a body that holds an inherited story about what money is and is not for. We all need someone to do hard things with, and shame disappears when you share it.

Literacy can be googled. Legitimacy, permission, and a peer cannot. They have to be built, with other people who get it without you having to explain.

Why I am writing this today.

We partnered with The Bloom on a scholarship to make sure our DearMoney program reaches the people who would otherwise not be able to join. The June 2026 cohort applications close on 15 May. So don’t hesitate: if you have read this far and at any point thought that’s me, apply for the chance to receive a fully funded place in the DearMoney program.

You do not need a polished story to apply. The applications I cannot stop thinking about are the honest and raw ones. The Karachi-based applicant who opened with “felt like ranting today.” (SAME). The applicant in Berlin who simply wrote, “I have no income right now.”

It is a simple process that should not take too much of your time, and if nothing else, if you do not join the program, you will still contribute to the overall purpose of our work together. To make others feel like they are not alone.

The other way - join and support

Some of you reading this may not recognize yourself in these stories. That does not mean you don’t need support. Maybe you grew up with parents who explained a mortgage, or a country whose currency stayed put, or a family where money was something you learned about. But your relationship with money may still need a lot work, because you hold deep anxiety and fear around money, and DearMoney is built for you too.

If that’s you, here is something I want to be open about: the only reason the scholarships exist is because other people pay to join the programs. There is no foundation behind this work, no grant. Every scholarship seat is funded by the people who join directly or sponsor a spot for someone who needs it.

It is the same logic I wrote about last month. The chama, the friendship account, the seettu. You put in what you have so the next person can pull out what they need.

So if you read this letter and are interested in doing the work, you are deeply welcome:

Warmest,

Gauri

Founder and ED, DearMoney

P.S. If your friend, sister, cousin, or colleague is the first something in their family to navigate this work, please forward this letter to them.